Calculate income, taxes, and more with these job flash cards.

There are 28 flash cards in this set (7 pages to print.)

To use:

1. Print out the cards.

2. Cut along the dashed lines.

3. Fold along the solid lines.

Sample flash cards in this set:

| Questions | Answers |

|---|---|

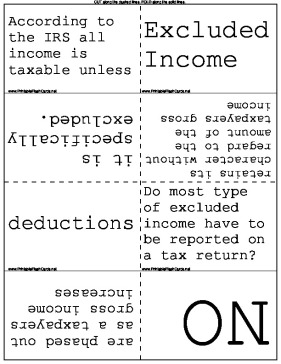

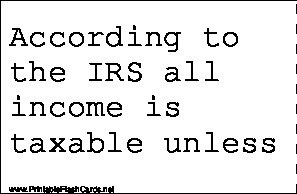

| According to the IRS all income is taxable unless | it is specifically excluded. |

| Excluded Income | retains its character without regard to the amount of the taxpayers gross income |

| deductions | are phased out as a taxpayers gross income increases |

| Do most type of excluded income have to be reported on a tax return? | NO |

| Gross Income | all income a taxpayer receives in the form of money, goods, property, and services that is not exempt from tax. This also includes other forms of compensation such as fringe benefits and stock options |

| Adjusted Gross Income (AGI) | subtract from gross income certain specific deductions or adjustments - these deductions include IRA, certain expenses for self employed, alimony payments, and moving expenses |

| Taxable Income | subtract additional deductions (standard or itemized) and exemptions from AGI |

| How to calculate Taxable Income and Tax liability | Start with Gross Income Minus Adjustments to Income (above line deductions) = AGI Minus greater of itemized deductions or standard deduction MINUS personal and dependency exemptions=Taxable Income*Tax Rate - Gross tax Liability MINUS credits = net tax liability or Refund Receivable |

| What is Earned Income? | income is received for services performed Ex - wages, salaries, tips, professional fees or self employment income |

| What is Unearned Income? | interest, dividends, retirement income, alimony and disability income |

| What income is subject to FICA taxes? | Earned income Unearned income is NOT subject to FICA |

| What is the Doctrine of Constructive Receipt? | that cash based taxpayers be taxed on income when it becomes available, regardless of whether it is actually in their physical possession. But the funds must be available without substantial limitations. |

| When is income considered to have not been constructively received? | if a taxpayer declines it, as in the case of a prize or an award or if there are significant restrictions on the income or if the income is not accessible to the taxpayer. |

| Under claim of right doctrine... | income received without restriction must be reported in the tax year received, even if there is a possibility it may have to be repaid in a later year. |

| When does the taxpayer have to report income that had to be repaid? | the repayment is deductible in the year repaid. As a result the taxpayer is not required to amend his reported gross income for the earlier year. |

| What are the 2 categories IRS classifies workers? | 1. Employees 2. Independent contractors |

| How much does a self employed taxpayer earn before he must file a tax return? | $400 |

| What schedule are self employed income reported on? | Schedule C Profit or Loss from Business |

| What schedule do farmers or fisherman report their income? | Schedule F, Profit or loss from farming |

| Self employment income also includes: | 1. Income of ministers, priests and rabbis for performance of services of baptisms and marriages 2. distributive share income allocated by a partnership to its general partners or by a limited liability company to its members reported on Schedule K-1 |

| What is the tax rate for Social Security and Medicare? | 15.3% up to $113,700 of a taxpayers combined earned income. |

| what is the rate of SS and Medicare once earned income exceeds $113,700? | a rate of 2.9% representing only the Medicare portion applies to the excess earnings. There is no cap to the 2.9% tax. |

| What are the 2 adjustments to the self employment tax that reduce overall taxes for a taxpayer with self employment income? | 1. the taxpayers net earnings from self employment are reduced by 7.65%. Just as the employers share of SSC is not considered wages to the employee, this reduction removes a corresponding amount from the net earnings before the SE is calculated 2. the taxpayer can deduct the employer equivalent portion of his self employment tax in determining his AGI |

| What schedule is self employment tax calculated on? | Schedule SE |

| Can married taxpayers combine their income or loss from self employment to determine their individual earning subject to SE tax? | NO |

| Form 8919 Uncollected Social Security and Medicare Taxes on Wages | Form that is filed by employees if their employer fails to withhold ss and Medicare taxes. |

| When does an employee have to recognize an advance wages, commissions or other earnings? | the year it was constructively received regardless of whether he has earned the income. |

| What are supplemental wages? | compensation that is paid to an employee in addition to his regular pay. |